Suite à une grève chez bpost il n'est temporairement pas possible de choisir pour livraison à domicile ou à une autre adresse. Besoin de quelque chose en urgence ? Choissisez pour retrait en magasin ou passez plutôt dans un magasin Club à proximité.

- Retrait gratuit dans votre magasin Club

- 7.000.000 titres dans notre catalogue

- Payer en toute sécurité

- Toujours un magasin près de chez vous

Suite à une grève chez bpost il n'est temporairement pas possible de choisir pour livraison à domicile ou à une autre adresse. Besoin de quelque chose en urgence ? Choissisez pour retrait en magasin ou passez plutôt dans un magasin Club à proximité.

- Retrait gratuit dans votre magasin Club

- 7.000.0000 titres dans notre catalogue

- Payer en toute sécurité

- Toujours un magasin près de chez vous

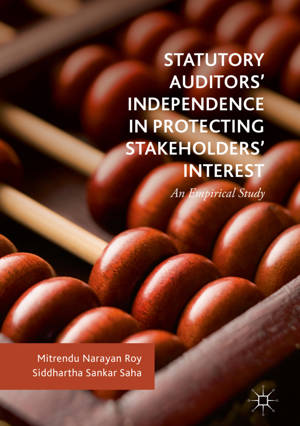

Statutory Auditors' Independence in Protecting Stakeholders' Interest

An Empirical Study

Mitrendu Narayan Roy, Siddhartha Sankar Saha

Livre relié | Anglais

210,95 €

+ 421 points

Format

Description

- Comprises a cross country analysis of regulatory and ethical framework for statutory auditors' independence which is not made in studies seen so far;

- Incorporates comparative analysis of statutory auditors' independence in select corporate accounting scandals from different countries across the globe which has not been seen in past studies;

- Examines empirical analysis of primary data collected based on opinions of respondents.

Spécifications

Parties prenantes

- Auteur(s) :

- Editeur:

Contenu

- Nombre de pages :

- 517

- Langue:

- Anglais

Caractéristiques

- EAN:

- 9783319737263

- Date de parution :

- 25-08-18

- Format:

- Livre relié

- Format numérique:

- Genaaid

- Dimensions :

- 148 mm x 210 mm

- Poids :

- 1038 g